Set for release in November 2023, the Study on the Economic Potential of Far Edge Computing in the Future Smart Internet of Things has been led by DECISION Etudes & Conseil for the DG CONNECT with the objective to assess the economic potential and environmental impacts of a paradigm shift in the domain of the Internet of Things (IoT) towards computing at the Edge.

Reading time: 4 min

More computing capacity spurs decentralisation and edge intelligence.

The Internet of Things (IoT) has experienced exponential growth in recent years, resulting in the deployment of billions of devices in our surroundings. It is a source of a vast amount of heterogeneous data, generated at the edge of the network. All of this requires processing power and storage, lots of it.

Edge computing applications, particularly high-value analytics, high-performance processors and artificial intelligence, delivered via machine learning (ML), allow massive data to be processed near its source. Overall, edge intelligence provides a promising solution to the challenges posed by the exponential growth of IoT devices and the increasing need for real-time data analysis and decision-making in key economic sectors, essential for Europe’s competitiveness.

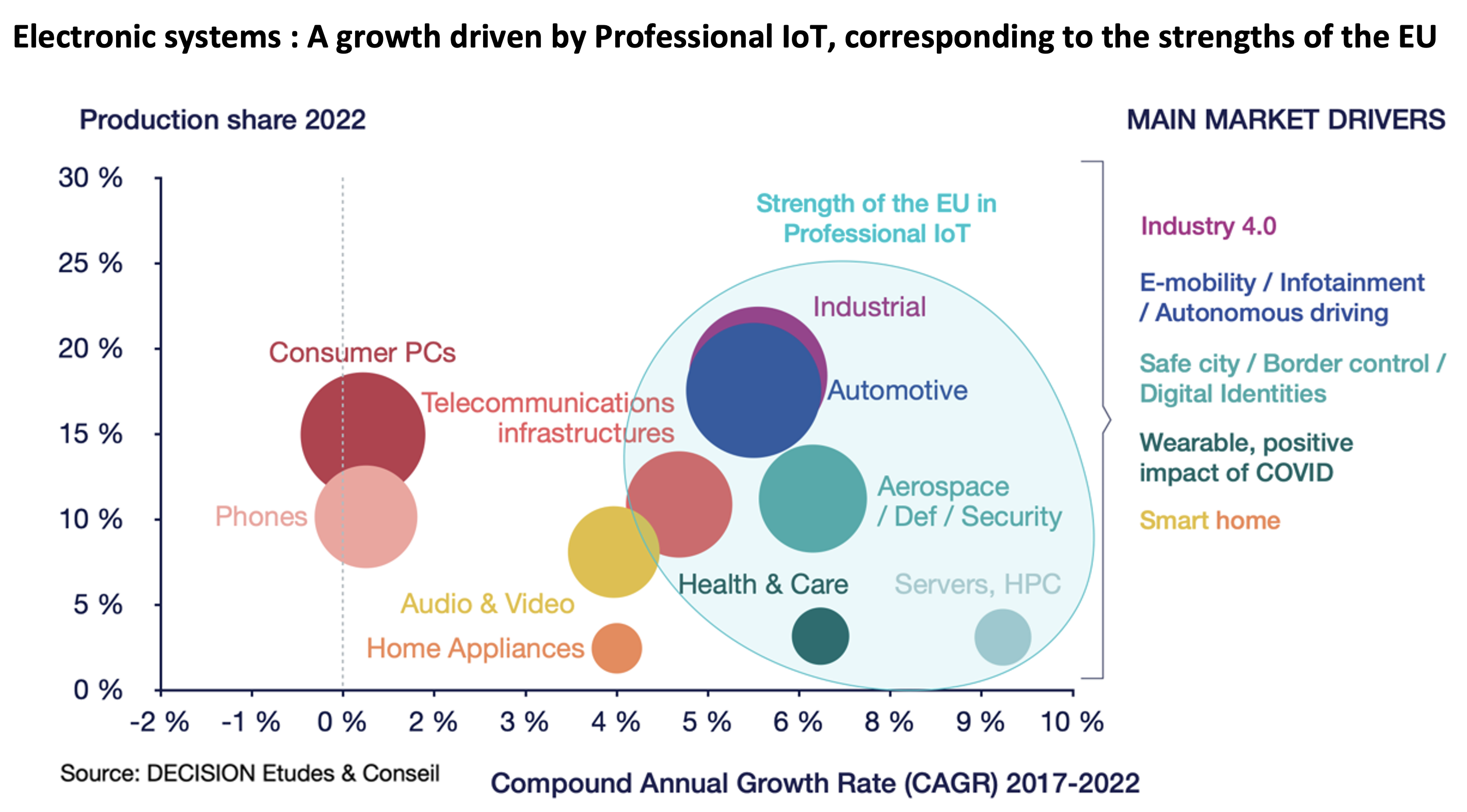

Professional IoT exceeds the market of consumer IoT.

Since 2021, the Professional IoT market[1] exceeds the one of consumer IoT (smartphones, consumer PC, etc.). In addition, professional IoT markets are driving the global growth of ICT, with +7%/year forecasted from 2021 to 2027.

The EU manufacturers of professional IoT own 28% global market shares in 2021, in first position ahead of Other Asia (22%), China (21) and the USA (20%).

However, these market shares are decreasing over years due to the shift of the market towards Asia and the rise of Asian manufacturers. In terms of production location, the outsourcing trend already led to only 20% of professional IoTs being produced on the EU soil in 2021.

Source: DECISION Etudes & Conseil – Study on the Economic Potential of Far Edge Computing in the Future Smart Internet of Things (DG CONNECT – 2023)

The Edge will Eat the Cloud

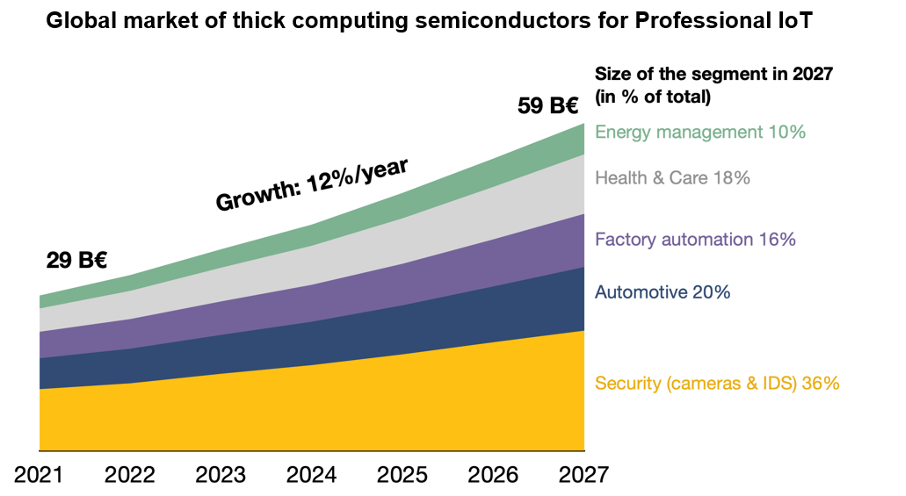

Edge computing in Professional IoT will generate a global growth of nearly 88B€ by 2027: 40B€ in semiconductors ensuring computing functions at the micro-edge, and 48B€ in the construction and deployment of local datacenters.

From 2021 to 2027, the installed base of professional IoT in the World will move from 69B to 92B (x1.3). The volume of data processed by these IoT will move from 15ZB to 38ZB (x2.5).

Furthermore, by 2027, 52% of the data will be processed in the micro-edge, 29% in the far edge and 19% in the cloud. In our definition of edge computing (micro-edge and far edge), then 81% will be processed at the edge.

Industrial IoT Needs an Open Edge Platform

The emergence of decentralised intelligence and automation in future infrastructures will spur the need for lightweight frameworks and open platforms which are expected to create ample opportunities for edge computing vendors.

These advantages can be beneficial in various application domains, including connected and automated vehicles, smart health, intelligent transportation systems, and factory automation (including industrial robotics), energy management IoT (building and city automation, smart grids, smart charging stations), security IoT, connected health & care devices, asset trackers for logistics and agriculture.

The building of Cloud-to-edge IoT platforms are a key driver of this growth (cloud & edge models will co-exist in hybrid models). It is a key growth opportunity for the EU IoT manufacturers but also a threat as mastering not only the manufacturing of IoT, but also the new bricks of this emerging value-chain are challenging and lead to the apparition of many newcomers:

- US cloud hyperscalers, but also telecommunication operators, are deploying Cloud and Edge IoT platforms.

- Semiconductor providers are gaining importance. At the semiconductor level, the economic impact will mainly benefit to applications based on “thick computing[2]” (82%) where US & Taiwanese companies have a strong leadership.

One major challenge, however, is linked to the fact the Industrial IoT is not a homogeneous thing, but rather a fragmented collection of technologies based on embedded systems and machine-to-machine communications across different vertical applications.

Current Industrial IoT systems rely on a myriad of proprietary and open-source software platforms, using a vast range of communication technologies to connect endpoints and applications in both greenfield and brownfield (legacy) deployments. IIoT designers are forced to become familiar with a plethora of tool sets, application development environments, operating systems, connectivity types — including both standard and proprietary protocols — cybersecurity aspects and industry-specific standards.

As such, one of the biggest barriers to wider integration of edge platforms is the lack of interoperability and standardization between different systems and technologies. While these platforms have the potential to provide benefits to both the industry and the end users, it requires an open platform approach driven by key stakeholders of the value chain to share upfront costs for hardware installation, ongoing maintenance, and service provision, to offer viable commercial services.

The edge is emerging as an entirely new ecosystem within industrial internet-enabled architectures and Cyber Physical Systems.

The edge is up for being more muscled

More computing capacity at the edge offers several advantages, such as increasing the intelligence at the edge, decentralising data aggregation and analytics as well as real-time decision-making and local control. With the evolution of next generation microprocessor chips (incl. MP SoCs, chiplets, System-in-a-Package, etc.), edge AI processors and energy-efficient computing architectures, advanced systems functions can be realised, such as reduced response time, lowered network traffic and congestion, optimized resource utilization, improved bandwidth, and enhanced privacy.

Thick computing semiconductors are processors and memories designed to perform high-rate data processing (>100 Tops).

Source: DECISION Etudes & Conseil – Study on the Economic Potential of Far Edge Computing in the Future Smart Internet of Things (DG CONNECT – 2023)

According to DECISION’s estimates, the demand for thick computing semiconductors associated with the European end-user industries in professional IoTs (automotive, factory automation, etc.) will represent by 2027 the equivalent of the global sales of Nvidia in 2021… In other words, there is room within the European market to sustain the emergence of a European Nvidia among the 12-15 startups involved in this segment, in addition to NXP and Bosch.

However, so far this EU market benefits in its large majority to US players building partnerships with EU professional IoT manufacturers (such as the partnerships between Qualcomm and Volkswagen, BMW, Stellantis…).

The Promise of Edge Computing being more environmentally friendly.

The overall environmental impacts associated with the global deployment of professional IoT (devices, network, and storage) represents 33% of the impact of the whole Information Communication and Technology sector (ICT) in 2021. With the booming of the number of Professional IoT and associated data, the environmental impact of the global installed base of industrial IoT will double in 6 years.

In principle, edge computing will avoid central processing and therefore excess energy consumption through saturated network and internet traffic. However, by 2027, the shift towards edge computing in professional IoT will not significantly reduce the environmental impacts of professional IoT due to a re-bounce effect. Indeed, the positive aspects of edge architectures (data processing directly at the micro edge + avoid energy for transport networks towards clouds) are to a large extent compensated by the negative aspect of high-performance computing architectures at the edge with an increasing carbon footprint. The second negative aspect of edge comes from the fact that computing in local datacenters is less efficient and overall has higher impacts than in hyperscalers cloud computing.

The situation of decentralised edge infrastructure may reconcile if 1) the processing capacities of embedded devices is significantly reduced, restraining certain usages requiring too much processing capacities for non-critical applications and 2) if whenever possible data remains processed and stored directly at the micro-edge, without deployment of local datacenters nor clouds.

To know more, download the full study: Study on the Economic Potential of Far Edge Computing in the Future Smart Internet of Things (DG Connect 2023)

[1] Automotive electronics, factory automation (including industrial robotics), energy management IoT (building and city automation, smart meters, smart charging stations), security IoT, connected health & care devices, asset trackers for logistics and finally IoT for agriculture.

[2] Thick computing semiconductors are processors and memories designed to perform high-rate data processing (>100 Tops).